Burr Type XII|

Probability density function  |

|

Cumulative distribution function  |

| Parameters |

|

|---|

| Support |

|

|---|

| PDF |

|

|---|

| CDF |

|

|---|

| Quantile |

|

|---|

| Mean |

where Β() is the beta function where Β() is the beta function |

|---|

| Median |

|

|---|

| Mode |

|

|---|

| Variance |

|

|---|

| Skewness |

|

|---|

| Excess kurtosis |

where moments (see) where moments (see)  |

|---|

| CF |

![{\displaystyle ={\frac {c(-it)^{kc)){\Gamma (k)))H_{1,2}^{2,1}\!\left[(-it)^{c}\left|{\begin{matrix}(-k,1)\\(0,1),(-kc,c)\end{matrix))\right.\right],t\neq 0}](https://wikimedia.org/api/rest_v1/media/math/render/svg/4d57864ffe50078a34292d9f949f09e0f47ab2b3)

where  is the Gamma function and is the Gamma function and  is the Fox H-function.[1] is the Fox H-function.[1] |

|---|

In probability theory, statistics and econometrics, the Burr Type XII distribution or simply the Burr distribution[2] is a continuous probability distribution for a non-negative random variable. It is also known as the Singh–Maddala distribution[3] and is one of a number of different distributions sometimes called the "generalized log-logistic distribution".

Definitions

Probability density function

The Burr (Type XII) distribution has probability density function:[4][5]

![{\displaystyle {\begin{aligned}f(x;c,k)&=ck{\frac {x^{c-1)){(1+x^{c})^{k+1))}\\[6pt]f(x;c,k,\lambda )&={\frac {ck}{\lambda ))\left({\frac {x}{\lambda ))\right)^{c-1}\left[1+\left({\frac {x}{\lambda ))\right)^{c}\right]^{-k-1}\end{aligned))}](https://wikimedia.org/api/rest_v1/media/math/render/svg/a3c758cb4945e4a43a37fb66ad628b53ca8de40c)

The  parameter scales the underlying variate and is a positive real.

parameter scales the underlying variate and is a positive real.

Cumulative distribution function

The cumulative distribution function is:

![{\displaystyle F(x;c,k,\lambda )=1-\left[1+\left({\frac {x}{\lambda ))\right)^{c}\right]^{-k))](https://wikimedia.org/api/rest_v1/media/math/render/svg/00238e8a5ecdca4563db2344bfca37b93baee67f)

Applications

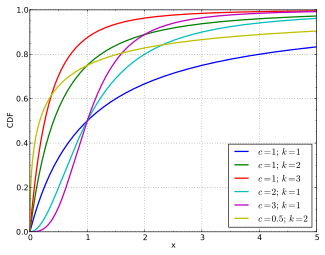

It is most commonly used to model household income, see for example: Household income in the U.S. and compare to magenta graph at right.

![{\displaystyle X=\lambda \left({\frac {1}{\sqrt[{k}]{1-U))}-1\right)^{1/c))](https://wikimedia.org/api/rest_v1/media/math/render/svg/4d1a4bbf6d1e2310503982df8976c74f71d19d70)